- Commercial & Contract Disputes

- Company & Shareholder Disputes

- Construction Disputes

- Contentious Trusts & Probate

- Energy and Oil & Gas Disputes

- Injunctions & Emergency Interim Relief

- Financial Services Disputes

- Fraud & Asset Tracing

- Intellectual Property & Technology Disputes

- International Litigation & Arbitration

- Judicial Review

- Mediation & Other ADR

- Litigation Property Disputes

- Public Procurement Challenges

- Tax Disputes

- Commercial & Contract Disputes

- Company & Shareholder Disputes

- Construction Disputes

- Contentious Trusts & Probate

- Energy and Oil & Gas Disputes

- Injunctions & Emergency Interim Relief

- Financial Services Disputes

- Fraud & Asset Tracing

- Intellectual Property & Technology Disputes

- International Litigation & Arbitration

- Judicial Review

- Mediation & Other ADR

- Litigation Property Disputes

- Public Procurement Challenges

- Tax Disputes

Home // Insights & Events // Chancellor announces immediate changes for Capital Gains Tax (CGT)

Chancellor announces immediate changes for Capital Gains Tax (CGT)

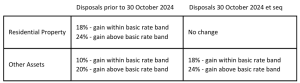

The Autumn Budget saw an immediate increase to the rates for Capital Gains tax:

This brings the rates for gains on all other assets in line with the rates for gains on residential property. Whilst these changes are less considerable than had been rumoured, there are also a few notable changes to CGT reliefs and a new anti-avoidance measure in relation to limited liability partnerships.

Investors’ Relief

The relief allows for a lower rate of CGT on disposals of unlisted trading company shares subject to certain conditions being met. Tax was charged at the rate of 10% on qualifying gains of up to a lifetime limit of £10 million. For disposals on or after 30 October 2024, the lifetime limit is reduced to £1 million. Additionally, from 6 April 2025 the rate rises to 14% and then 18% with effect from 6 April 2026.

Where a share reorganisation occurs, qualifying shareholders could elect to crystallise a gain at the point of the election to “lock in” the lower CGT rate. Following the changes, when shareholders continue to meet the qualifying conditions on 30 October 2024 and make an election on or after 30 October, those gains will be subject to the new £1 million lifetime limit.

Business Asset Disposal Relief (BADR)

As with Investor’s relief, the rate of CGT for qualifying disposals of business assets will increase to 14% with effect from 6 April 2025 and 18% from 6 April 2026. The lifetime limit has been £1 million since 2020. This will represent an increase of £80,000 for disposals in excess of £1 million from 6 April 2026.

Anti Avoidance – Liquidation of Limited Liability Partnerships

A new anti-avoidance measure is introduced with effect from 30 October 2024. Prior to this change, assets held by Limited Liability Partnerships (LLP) were treated as if held by members of an ordinary partnership. As a result, no gains accrued when assets were contributed to the LLP. This treatment ceased to apply on the appointment of a liquidator, but cessation did not give rise to a disposal of assets by the LLP members.

The new legislation will deem that a disposal arises when an LLP is liquidated and assets a member has contributed are disposed of to the member, company or other person connected to that member. The amount of the chargeable gain will be the amount equal to what accrued at the time the member contributed the asset to the LLP.

Planning

Many family trading company shares qualify for BADR and Business Property Relief (BPR) for Inheritance Tax. A lifetime transfer of qualifying shares into a settlement/trust would obtain 100% relief on £1million and an effective IHT rate of 10% thereafter, which is less than CGT at 18%. Certainly something to think about!

For advice on how the changes may affect you or your business and for potential planning opportunities, please contact Roger Harding.

Related articles

This update is for general purposes and guidance only and does not constitute legal or professional advice. You should seek legal advice before relying on its content. Greenwoods Legal LLP is a Limited Liability Partnership, registered in England, registered number OC306912. Our registered office is Queens House, 55-56 Lincoln’s Inn Fields, London, WC2A 3LJ. A list of the members’ names is available for inspection at our offices in Peterborough, Cambridge and London. Authorised and regulated by the Solicitors Regulation Authority, SRA number 401162. Details of the Solicitors’ Codes of Conduct can be found at www.sra.org.uk. All instructions accepted by Greenwoods Legal LLP are subject to our current Terms of Business. VAT Reg No: 161 9287 89.

Get in touch with us (*Required fields)

Sign up to updates (*Required fields)